As you consider the farm business legacy and transition plan, it can seem rather daunting. There are a lot of details involved. Sometimes it helps to step back and understand the big picture.

As you consider the farm business legacy and transition plan, it can seem rather daunting. There are a lot of details involved. Sometimes it helps to step back and understand the big picture.

Regardless of the particulars of your specific farm business, a basic strategy can usually help you wrap your head around the work that needs to happen regarding the farm transition plan.

In general, there are a few things you need to do:

- Provide lifetime income for the retiring generation;

- Provide control of the farm business to the successor generation in a way that is:

- Affordable to the buyer;

- Fair to the retiring generation; and

- A minimal tax burden to everybody.

- Provide an equitable division of the family estate when the last of the retiring generation passes away.

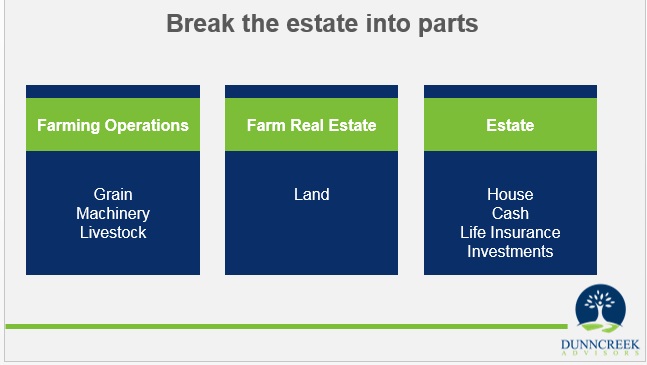

Farm Operations

For the successor:

- Create an entity that owns the farming business: the equipment, the grain in storage, the facilities, the livestock, etc.

- Buy the entity from the retiring generation at 75% of fair market value.

- Gives the successor a better chance to succeed.

- Reduces the capital gains tax paid by the retiring generation as they sell the business.

- Paid over 7 years as a lease to own. This allows the payments to be deducted as a business expense by the successor and received as ordinary income instead of as:

- Self-employment income subject to FICA tax; or

- Capital gains tax at cap gains rates.

Farm Real Estate

For all the heirs in the family:

- Income for life for the retirees;

- Transfers at death with a step-up in cost basis to eliminate cap gains tax;

- Legal entity can be created to dictate the sale of the land among the heirs:

- Set a favorable price for the successor heir;

- Set favorable sales terms for the timing of the sale for the successor heir; or

- Can provide income for all heirs instead of a quick sale.

Residual Estate

For all heirs in the family:

- Most assets are easily liquidated and divided;

- Legal instruments can be used to equalize the inheritance to all heirs;

- If most of the farmland is inherited by the successor then, most of the residual estate would go to the non-successors to equalize.

- If additional assets are required to equalize the estate, they can be provided with life insurance.

- Life insurance may help:

- As long as retiring generation is fairly healthy they could be insured.

- Second to die insurance can be pretty affordable. Often $16,000 in annual premiums will yield $1M in death benefit.

- An Irrevocable Life Insurance Trust (ILIT) can keep the death benefit out of the estate and avoid estate taxes.

If you find yourself thinking about the big picture of your farm business transition and would like to talk, schedule a time for us to talk HERE. I am always happy to meet with people who are working on their transition plans. Dunncreek Advisors does not provide legal or tax advice, nor is this article intended to do so.