When the market falls 6 percent in one day, it most likely feels like you need more cash on hand than usual. Conversely, when the market is climbing 45 percent in roughly 60 days you may decide you want to dump everything in the market and have nothing in cash.

This situation illustrates one of the realities of human nature. Humans are herd animals. We like to go with the group. And we tend to suffer from recency bias. That is, we expect whatever just happened to keep happening. When things are good, we expect them to stay good. When they are bad, we expect them to stay bad.

When it comes to investment markets, our human nature can do us harm. Investment prices are volatile. They move UP and DOWN often. Usually, nobody sees the big moves coming.

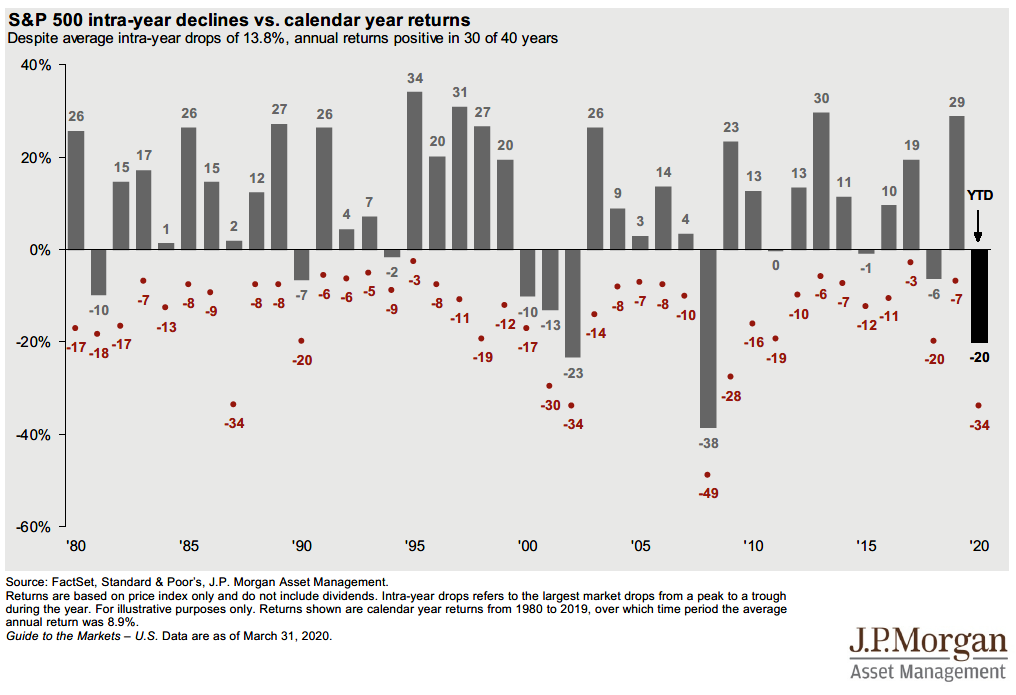

This chart illustrates that since 1980, the S&P 500 index posted a drop of 13.8 percent from the prior year end on average every year. And, at the same time, the S&P 500 index has averaged 11.06 percent growth per year with dividends reinvested over time. So if you wait and keep score over the longer term, you will get the long-term average growth rate.

So if you listen to your instincts, you are likely to sell after a loss and buy back in after a rebound. If you sell low and buy high, you will eventually run out of money. All the while the stock market was willing to deliver you 11 percent growth.

This is a spot where professional advice can be extremely valuable. Understanding how much of your money needs to be safe and accessible for a short-term need, and what money should be invested for long-term growth is a critical decision, and making this decision can be very hard to do on your own.

Everybody needs a cash reserve. It will give you flexibility when unexpected or bad things happen. The amount of cash you should have available will depend on your situation, and should be based on your needs and goals. It should NOT be based on current investment market conditions, or your opinion about future investment market conditions.

Remember that cash in your savings account at the bank is not an investment. It does not grow. It’s insurance. It’s not supposed to grow. It is supposed to protect you from a bad thing that you hope to avoid, yet know is pretty common and can be a real pain if you are not ready when it comes.

To decide how much “Emergency Money” you need consider these two factors:

- How likely is it that your income will stop on short notice? Do you work in a volatile industry like advertising where people get laid off on short notice through no fault of their own? Do you work in direct sales where your territory could be cut, or contract terminated with little notice? If you have HIGHER risk of unexpected lay off, then you need MORE Emergency Money.

- How long will it take you to find another job as lucrative as the one you have now? Would you be able to do something temporarily or part time while you worked to find a new job, and if so how much would that bring in? If it would be hard to find a job that matches your current salary, or you work in a field where new opportunities are rare, you will need more emergency money.

So, you start with enough money to cover 90 days worth of essential bills — those things you can’t do without each month.

Then if you have a higher chance of getting laid off without notice, add another 90 days to that.

If you have a high paying job that will take awhile to replace should you lose it, you might need to double the amount up to 12 months of bills.

So for instance if you spend $5,000 each month on basic expenses, then you will need:

- 90 days money = $15,000

- 6 months money = $30,000

- 12 months money = $60,000

If you need any assistance understanding your basic expenses, follow this link. You will find a great resource to track your basic income and expenses.

The idea is to have a pool of funds at hand that will allow you to pay your rent, put gas in the car, support your family, eat and have clean clothes for job interviews until you find the new job. A few thousand dollars will also make it easier when unexpected expensenses come up like when your kid breaks an arm and you have a $2,000 co-pay at the emergency room, or when the car needs new brakes and tires and you have a $1,500 repair bill.

Many clients tell me they hate the idea of having so much money in savings at the bank earning NO interest. Remember, this is not an investment, it’s insurance against a financial emergency. Not earning interest is a small price to pay to have those funds easily accessible if the need arises.

However, I often suggest an option to families that own a home. You can keep half the money in the bank and the remainder of your emergency fund can be held in the equity in your home. I suggest using a Home Equity Line of Credit (HELOC) for this purpose. You can set up a HELOC for a modest application fee at your local bank. When approved, you have the bank’s agreement to loan you money with an interest rate that is based off the prime interest rate at the time you borrow the money. The loan is secured by the equity in your home. The interest rate is usually much less than a cash advance on your credit card.

The advantage of the HELOC, is that you have favorable terms if you need to borrow the money. And, you have the equity in your house compounding until such time as you actually need it for an emergency. The money is easy to get at when you need it and you do not need permission to get the money when you are in a jam.

Even after all this, it can be tricky to understand how much cash you really need. That’s why I always suggest that a great place to start improving your cash reserve strategy is to talk with a couple of CERTIFIED FINANCIAL PLANNER™ professionals.To find a CFP® professional near you, start your search here.

As you visit with financial planners, I suggest a couple things to check:

- Is the advisor always the client’s advocate – in other words a fiduciary advisor?

- Is the advisor only paid by clients, not any financial product manufacturer or distribution network? This is called a fee-only advisor.

These two points help assure that you are working with a professional who is committed to your best interest at all times. It may seem sort of obvious that a professional would work in this way, but it’s certainly not automatic.

A fiduciary, fee-only, CFP® professional can help you make great retirement income choices and develop a comprehensive financial plan that is driven by your goals and priorities and addresses all aspects of your financial life. With a big-picture approach, you will be better prepared to understand your options at every step along the way.

I am a CFP® professional. I’m always a fiduciary and I only work on a fee basis. And I’m still taking on a few great families to be part of my financial planning practice so if this article has you thinking about your own circumstances, contact my office at rdunn@dunncreekadvisors.com. I am always happy to meet with people who are working on their retirement plans.

Dunncreek Advisors does not provide legal or tax advice, nor is this article intended to do so.

14 retirement mistakes to avoid

14 retirement mistakes to avoid